Amidst all the chatter about deflation, Daniel Gross over at Newsweek reminds us that deflation can emerge for two very different reasons: (1) a collapse in aggregate demand or (2) a surge in aggregate supply. This distinction is an important one that is often overlooked when it comes to conduct of monetary policy. Before getting into the policy implications, though, let's look at how these two forms of deflation are different. Here is how Gross describes deflation coming from a collapse in aggregate demand:

The second type of deflation is the result of positive aggregate supply shocks. Here is how Gross explains this form:

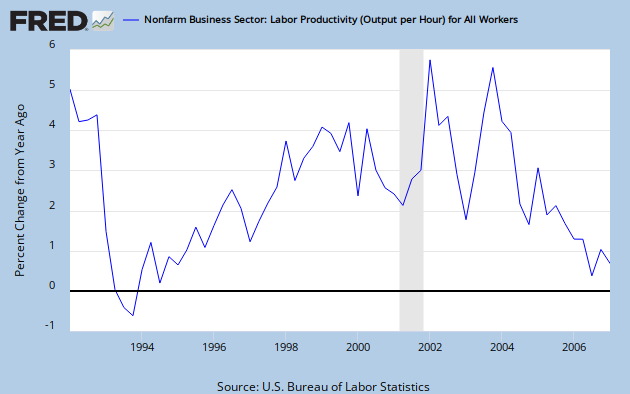

I bring these differences up because it seems clear to me that one of key reason we are this mess now is that the Fed in the early-to-mid 2000s failed to make this distinction. It saw the deflationary pressures of that time as indicating the harmful, demand-induced form when in fact they were the result of the rapid productivity gains at that time. Here is one graph the makes my point:

This figure shows that the growth rate of domestic demand started accelerating in mid-2002 and continued increasing through late 2004. There were no signs of collapsing demand here. Yet the Fed still saw a threat of demand-induced deflation at least through late 2003. As a result, the Fed continued to push the federal funds rate lower and held it low until mid-2004. What the Fed ignored was that the productivity gains at the time were pushing down the inflation rate. The rest is history. (The Fed also got hung up on the negative output gap. But like the deflationary pressures, much of this gap was being driven the rapid productivity gains not a collapse in demand.)

This figure shows that the growth rate of domestic demand started accelerating in mid-2002 and continued increasing through late 2004. There were no signs of collapsing demand here. Yet the Fed still saw a threat of demand-induced deflation at least through late 2003. As a result, the Fed continued to push the federal funds rate lower and held it low until mid-2004. What the Fed ignored was that the productivity gains at the time were pushing down the inflation rate. The rest is history. (The Fed also got hung up on the negative output gap. But like the deflationary pressures, much of this gap was being driven the rapid productivity gains not a collapse in demand.)

Now in real time it may be hard to distinguish between aggregate demand-induced deflation and aggregate supply-induced deflation. For example, since the U.S. economy had just come out of the 2001 recession it is understandable why the Fed misread the deflationary tea leaves over 2002-2003. Fortunately, there is a way that makes it possible for monetary authorities to avoid making such mistakes: target aggregate demand or some measure of total spending. Stabilize this and the deflation distinction becomes a moot issue.

Read here for more on this issue.

Bad deflation is the kind we had in the Great Depression. "The last time we really had significant deflation in the U.S. was in the 1930s," notes Michael Bordo, professor of economics at Rutgers University. "Between 1929 and 1933, prices fell on average by 15 percent." This deflation was driven by a decline in output, demand, and credit—too little money and wages chasing too many goods and workers. The Depression-era cratering of wages and prices was disastrous because it rendered companies and consumers less able to pay their debts.There is no question this is type of deflationary pressures we experienced during the first half of 2009 and now face again in late 2010. The key to preventing such deflation is to stabilize aggregate demand via monetary policy. Lately, it appears the Fed has been failing to do just this.

The second type of deflation is the result of positive aggregate supply shocks. Here is how Gross explains this form:

But there have been periods of good deflation, in which prices fell even as the economy boomed. In the 1920s, known to this day as the roaring '20s because of the decade's economic vibrancy, prices fell about 1 percent per year. Between 1870 and 1896, prices fell consistently amid rapid economic growth—with plenty of booms and busts along the way. The reason: innovations like the railroad, the telegraph, electricity, and the assembly line helped farmers, entrepreneurs, and manufacturers to produce and ship their goods more cheaply and efficiently.As mentioned above, the distinction between these two forms of deflation is important when it comes to policy implications. The harmful form of deflation requires aggressive monetary easing to stabilize aggregate demand while the benign form does not. In fact, the benign form of deflation if driven by rapid productivity growth would imply, cetersis paribus, a higher neutral interest rate. Lowering the policy interest rate here would push market interest rates below the neutral rate, lead to excessive monetary easing, and too much current dollar spending. So no need for monetary or aggregate demand stimulus here. In short, both forms of deflation call for stabilizing aggregate demand.

I bring these differences up because it seems clear to me that one of key reason we are this mess now is that the Fed in the early-to-mid 2000s failed to make this distinction. It saw the deflationary pressures of that time as indicating the harmful, demand-induced form when in fact they were the result of the rapid productivity gains at that time. Here is one graph the makes my point:

This figure shows that the growth rate of domestic demand started accelerating in mid-2002 and continued increasing through late 2004. There were no signs of collapsing demand here. Yet the Fed still saw a threat of demand-induced deflation at least through late 2003. As a result, the Fed continued to push the federal funds rate lower and held it low until mid-2004. What the Fed ignored was that the productivity gains at the time were pushing down the inflation rate. The rest is history. (The Fed also got hung up on the negative output gap. But like the deflationary pressures, much of this gap was being driven the rapid productivity gains not a collapse in demand.)

This figure shows that the growth rate of domestic demand started accelerating in mid-2002 and continued increasing through late 2004. There were no signs of collapsing demand here. Yet the Fed still saw a threat of demand-induced deflation at least through late 2003. As a result, the Fed continued to push the federal funds rate lower and held it low until mid-2004. What the Fed ignored was that the productivity gains at the time were pushing down the inflation rate. The rest is history. (The Fed also got hung up on the negative output gap. But like the deflationary pressures, much of this gap was being driven the rapid productivity gains not a collapse in demand.)Now in real time it may be hard to distinguish between aggregate demand-induced deflation and aggregate supply-induced deflation. For example, since the U.S. economy had just come out of the 2001 recession it is understandable why the Fed misread the deflationary tea leaves over 2002-2003. Fortunately, there is a way that makes it possible for monetary authorities to avoid making such mistakes: target aggregate demand or some measure of total spending. Stabilize this and the deflation distinction becomes a moot issue.

Read here for more on this issue.

{kind=link}

{kind=link}

0 comments:

Post a Comment